No Down Payment Car Insurance in California

“Get instant no down payment car insurance in California!”

Compare Quotes in 2 Minutes

Powered by:

![]()

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Auto insurance in California has become one of the most frustrating household expenses for everyday drivers. Premiums keep rising year after year, making coverage for many residents unaffordable. Many drivers are looking for deals like no down payment car insurance in California. This type of policy allows someone to activate their policy and become legally insured with minimal upfront out-of-pocket expenses.

Many California drivers don’t have the funds to make a huge deposit on an insurance policy. For many people, the biggest problem isn’t the monthly payment, it’s the amount due when a policy is purchased. Even a car insurance policy under $100 a month can still be impossible to start if the insurer wants $400 or $500 upfront.

That’s why searches for no down payment car insurance in California continue to grow. Drivers aren’t trying to avoid paying for insurance. They’re trying to avoid a large upfront bill that can derail a budget instantly. Understanding how no-down-payment insurance really works in California is the key to getting legal coverage without unnecessary financial strain.

This guide explains what “no down payment auto insurance” actually means in California, how state laws shape your options, which drivers qualify for the lowest upfront costs, which insurers are typically cheapest, and how to avoid misleading $0-down advertising.

Why Californians Are Searching for No Down Payment Coverage

California auto insurance costs have increased sharply over the past few years. Repair costs are higher, medical claims are more expensive, and congestion in major metro areas leads to more frequent and more severe accidents. Even responsible drivers with clean records are seeing increases.

In cities like Los Angeles, San Diego, San Jose, Oakland, and San Francisco, full-coverage premiums commonly exceed $250 per month. When insurers also require a deposit equal to a portion of the policy term, the upfront cost can quickly reach several hundred dollars.

California is also a car-dependent state. Public transportation is limited in many regions, and driving is often essential for work, family obligations, and daily life. When coverage lapses or can’t be started quickly, drivers face fines, registration issues, and potentially much worse consequences.

For many Californians, the question is not “What’s the cheapest monthly policy?” It’s “What can I afford to start today?”

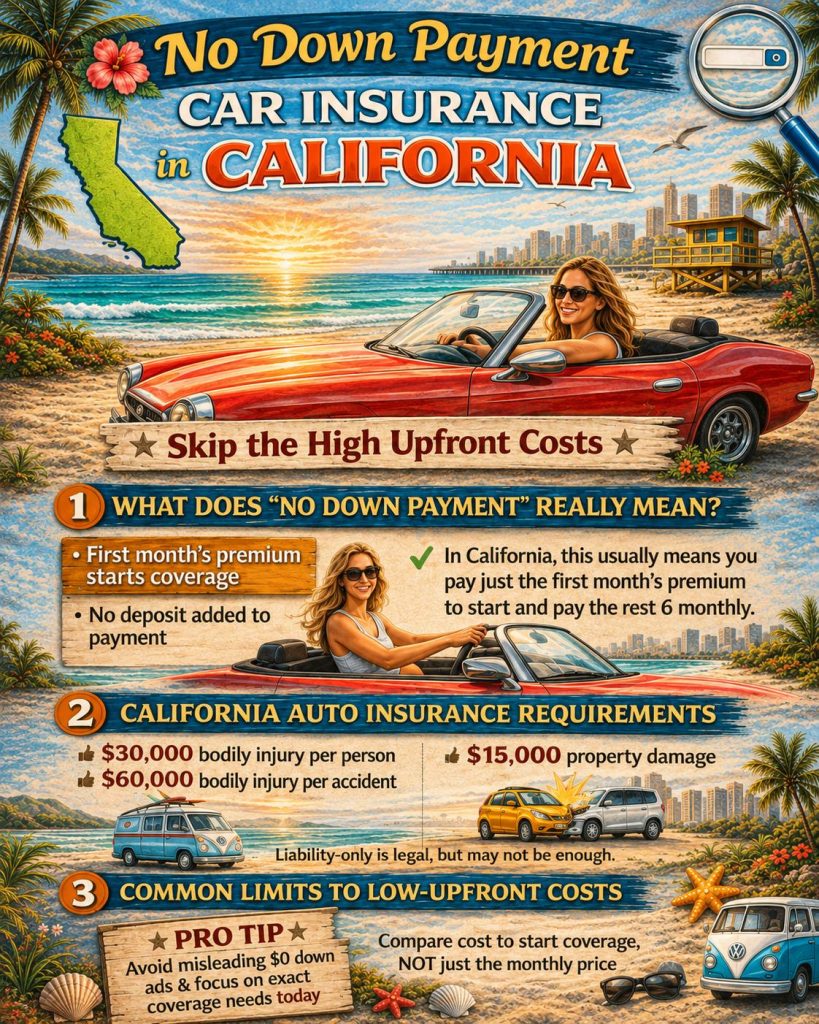

What “No Down Payment” Car Insurance Really Means in California

A true $0-paid-today auto insurance policy does not exist with legitimate insurers. Coverage begins immediately, and the insurer assumes financial risk the moment the policy is bound. Payment is required to activate coverage.

In California, “zero down car insurance” almost always means first-month-only billing. This structure allows you to start coverage by paying just the first month’s premium, without an additional deposit or percentage of the six- or twelve-month policy term.

Some insurers require 10% to 25% of the total premium upfront as a deposit. A first-month-only plan removes that extra charge and spreads the remaining balance across future payments, similar to how some instant auto insurance no down payment offers are structured.

The most important question to ask when shopping is simple: “What is the exact amount due today to start coverage?”

That number, not the advertised monthly price, determines whether a policy actually works for your budget.

California’s Minimum Auto Insurance Requirements

California is an at-fault state, meaning the driver who causes an accident is responsible for damages. This places heavy importance on liability coverage, which is a central part of vehicle insurance in the United States.

These minimums were increased to better reflect modern medical and repair costs. While they satisfy legal requirements, they still may not be sufficient in serious accidents.

Higher required limits increase the insurer’s immediate exposure, which can affect both monthly premiums and upfront billing requirements. Policies with higher limits often require more money collected early in the policy term.

California does not require Personal Injury Protection like Florida, but it does allow optional Medical Payments coverage. Adding optional coverages can raise both monthly and upfront costs.

Vehicle repair costs have exploded due to advanced driver-assistance systems, sensors, cameras, and proprietary parts. Even a low-speed collision can now cost thousands to repair.

Medical claims are also more expensive, and California’s legal environment can lead to higher settlement amounts. Dense urban traffic increases accident frequency, while theft and vandalism remain issues in many ZIP codes.

California also restricts the use of credit-based insurance scoring more than many states. Insurers rely more heavily on driving record, vehicle type, mileage, and territory, which can push prices higher in certain regions regardless of credit profile.

When expected losses rise, insurers respond by tightening underwriting and often requiring higher upfront payments.

How No-Down-Payment and Low-Down-Payment Plans Work in California

Low-upfront plans in California typically follow the same structure:

- First month’s premium due today

- Remaining balance billed monthly through a pay monthly car insurance structure

- Possible installment fees

Whether you qualify for first-month-only billing depends on your risk profile. Insurers evaluate factors such as:

- Driving history

- Prior insurance continuity

- Vehicle value and repair cost

- ZIP code and garaging location

- Coverage selection

Drivers with higher perceived risk often face deposits because insurers want more premiums collected before a claim can occur.

Who Qualifies for the Lowest Upfront Payments in California

Drivers most likely to qualify for first-month-only billing generally have:

- Continuous insurance history

- Clean or mostly clean driving records

- Moderate annual mileage

- Vehicles that are not expensive to repair

- Garaging locations with lower claim frequency

Because California limits the use of credit scoring, insurers often focus more heavily on driving behavior and territory when deciding billing flexibility.

Drivers Who Typically Face Higher Upfront Costs

Higher upfront payments are common for:

- Drivers with recent accidents or tickets

- DUI history

- New or inexperienced drivers

- Drivers with coverage lapses

- High-value or high-theft vehicles

- Dense urban ZIP codes

These drivers may still find affordable monthly premiums, but insurers often require more money upfront to manage early-term risk. In some cases, comparing low down payment car insurance options can be more realistic than looking only for true no-down-payment coverage.

SR-22 Insurance in California and Its Impact on Upfront Costs

An SR-22 is a certificate filed with the California DMV proving that you carry the required liability insurance. It is commonly required after DUI convictions, reckless driving, or driving without insurance.

SR-22 policies usually involve higher premiums and stricter billing rules. Many insurers require larger upfront payments or limit installment options for SR-22 drivers.

Maintaining clean driving and payment history over time is the best way to restore access to lower upfront billing structures.

Realistic Cost Examples for California Drivers

A 40-year-old driver in a suburban area with a clean record and an older sedan may see liability-only coverage under $100 per month and qualify for first-month-only billing.

A 25-year-old driver in Los Angeles with speeding tickets and a financed vehicle may face monthly premiums over $300, with a required deposit that raises the amount due today significantly.

A driver with a recent lapse may see a manageable monthly price but a much higher upfront payment. For some drivers, a $20 down payment car insurance option may be easier to qualify for than a policy advertised as $0 down.

In California, the “due today” number reflects perceived risk as much as price.

Five Cheapest No Down Payment Car Insurance Companies in California

The following insurers frequently rank among the cheapest in California and often allow monthly billing when drivers qualify.

Eligibility varies widely by driver and location, so comparing billing terms is essential.

How to Get the Lowest Amount Due Today in California

Start by focusing on the amount due today rather than the monthly price.

Ask whether the upfront amount includes a deposit. Choose coverage intentionally rather than defaulting to maximum limits. Ensure mileage and garaging information is accurate. Ask about autopay, paperless billing discounts, and whether you can secure car insurance with a checking account.

Avoid coverage lapses whenever possible. In California, a lapse can make low-down-payment options much harder to qualify for later.

How to Lower Both Upfront and Long-Term Costs

Drive a vehicle that is cheaper to repair and less likely to be stolen. Reduce mileage where possible. Maintain continuous coverage. Avoid tickets and at-fault accidents. Consider usage-based programs if you’re a safe driver, and compare buy now pay later car insurance options carefully if the amount due today is your biggest concern.

These habits improve both pricing and billing flexibility over time.

Avoiding Misleading “$0 Down” Ads in California

Be cautious of ads that only show a monthly price without clearly stating the amount due today. Avoid sellers who won’t provide written quotes or policy details.

Legitimate insurers can explain coverage, billing, and provide proof of insurance immediately after payment.

Special Considerations To Be Aware Of For California Drivers

California drivers face a different insurance environment than most states, and those differences directly affect how easy it is to qualify for low upfront or first-month-only billing.

Teen drivers in California are expensive to insure due to inexperience, dense traffic, and higher claim severity in urban areas. In most cases, adding a teen to an existing household policy is significantly cheaper than purchasing a standalone policy. Established household policies may also qualify for better billing terms, and families who own a home may want to compare bundle car and home insurance discounts to reduce overall costs.

Senior drivers often benefit from long insurance histories, lower mileage, and stable garaging locations. These factors can make it easier to qualify for monthly billing without a large deposit. However, rates can rise later in life depending on the insurer, so seniors should still compare billing structures carefully.

Low-income drivers in California may qualify for the California Low Cost Auto Insurance Program, a state-specific option designed to provide basic liability coverage at reduced rates. While it does not eliminate all upfront costs, it can significantly reduce both monthly premiums and the amount required to start coverage.

Rideshare and delivery drivers in California must pay close attention to coverage rules. Personal auto policies typically do not cover driving for companies like Uber, Lyft, or delivery platforms without an endorsement. Adding rideshare coverage increases premiums and often raises the upfront payment, so drivers should quote with insurers that explicitly support rideshare use to avoid billing surprises.

Compare Quotes in 2 Minutes

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

OUR WEBSITE

TRUST & AUTHORITY

Featured Articles

SEARCH

Looking for something specific? Use the search bar below to find answers to your questions!