Cheap Liability Car Insurance in NJ

Compare Quotes Today & Discover the Best Low-Cost New Jersey Auto Insurance Options.

Compare Quotes in 2 Minutes

Powered by:

![]()

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Bill Jones — insurance policy contributor

With rates rising for several years, many drivers in the Garden State are choosing cheap liability car insurance in NJ. New Jersey often ranks among the more expensive states for car insurance, especially for drivers in dense ZIP codes, drivers with lapses, and households with young or high-risk drivers.

The average annual cost of liability auto insurance in New Jersey can vary widely by ZIP code, driving history, age, vehicle, coverage choices, and insurer. Some consumer rate studies place liability-only coverage near the $1,000 to $1,200 annual range, but safe drivers with clean records who compare rates and qualify for multiple discounts may pay less. In some cases, drivers may find rates below $800 per year, but that is never guaranteed.

The truth is NJ’s high premiums reflect the risks of traffic congestion, theft, medical claims, and frequent accidents. With the right strategy found in this guide, you can still look for cheap liability car insurance in NJ without sacrificing essential coverage or misunderstanding the state’s minimum insurance rules.

Coverage note: CitizensInsurance.net is an independent insurance information and comparison website. It is not an insurance company, government agency, or official New Jersey state website. Rates, discounts, payment options, and eligibility vary by insurer, driver profile, policy, and state rules.

New Jersey’s Minimum Liability Laws

Every driver in New Jersey is legally required to carry auto insurance and be able to provide proof of insurance when operating a vehicle. New Jersey is somewhat unique compared to many other states because it offers two common policy structures: the Basic Policy and the Standard Policy.

New Jersey drivers should be careful when comparing liability-only quotes because the cheapest policy may also have the narrowest protection. The Basic Policy usually costs less, but it provides limited benefits. The Standard Policy is chosen by most New Jersey drivers because it offers broader coverage choices and the opportunity to buy higher limits.

Basic Policy

- Bodily injury liability is not included by default, although $10,000 of coverage for all persons, per accident, may be available as an option from some insurers.

- $5,000 for property damage liability per accident.

- $15,000 Personal Injury Protection (PIP) per person, per accident, with higher protection for certain serious injuries under state rules.

This option is cheaper but offers very limited protection. It may be best suited for drivers with few assets and few family responsibilities who are looking for the lowest possible premium. However, because liability limits are low, you risk being underinsured in the event of a serious accident.

Standard Policy Minimums

- $35,000 bodily injury liability per person.

- $70,000 bodily injury liability per accident.

- $25,000 property damage liability per accident.

- PIP coverage is available as low as $15,000 per person or accident, with higher limits available.

Most drivers choose the Standard Policy because it offers broader protection and more flexibility. Higher limits are also available and strongly recommended if you own property, have savings, or want stronger financial security after a serious accident.

Quick NJ minimum coverage reminder

For Standard Policies issued or renewed on or after January 1, 2026, New Jersey’s minimum bodily injury liability limits increased to $35,000 per person and $70,000 per accident, while the minimum property damage liability limit remains $25,000. The Basic Policy is separate and remains much more limited.

10 Companies Often Considered for Cheap Liability Car Insurance in New Jersey

While rates vary widely depending on driver profile, ZIP code, vehicle, coverage level, and claims history, these companies are often considered by New Jersey drivers shopping for liability-only coverage in NJ:

Known for competitive base liability premiums in many markets. It may be a practical option for drivers comfortable managing quotes and policies online.

Offers telematics programs like Snapshot, which may reward safe driving habits. Progressive may also be worth checking for drivers with minor tickets or mixed driving histories.

Often considered for policy bundling with home or renters coverage and local agent service. State Farm’s agent network may appeal to drivers who want more personal guidance.

May be competitive for drivers with clean records. Good driver, multi-policy, and other discounts can help reduce liability coverage costs for eligible customers.

This regional insurer is often considered by New Jersey drivers who prefer a company with local market experience. Depending on the ZIP code and driver profile, NJM may be competitive for liability coverage.

Popular in New Jersey and nearby states, with payment and coverage options that may appeal to drivers comparing liability pricing.

Discounts for safe driving, students, and certain households may help reduce costs. It can be worth checking for families with multiple cars or bundled policies.

Offers usage-based programs such as SmartRide in many states. It may also be useful for drivers comparing bundling home and auto coverage.

Available only to eligible military members, veterans, and qualifying families. For eligible drivers, USAA is often worth comparing for liability coverage.

May offer competitive liability rates for members, along with roadside assistance benefits. It can be a good comparison option for long-time NJ residents who already use AAA services.

The Overall Best and Cheapest Liability Auto Insurer in NJ

🥇 Strong Comparison Pick: GEICO Insurance

Often competitive • Easy online management • Broad availability

- Competitive rates for many liability-only shoppers

- Fast online tools for quotes and policy management

- Discounts that may apply to students, military members, and safe drivers

- Broad availability for drivers comparing national carriers

A widely available option to include when comparing New Jersey liability quotes

For many drivers in New Jersey, GEICO often stands out as a strong comparison option for liability-only coverage. GEICO’s rates may be competitive for drivers with clean records, and its online-first approach makes it easy to compare quotes, manage policies, and review discounts without relying heavily on local agents. Beyond affordability, GEICO offers broad availability and a wide range of discount programs that may apply to students, military members, and safe drivers.

While regional carriers like NJM and Plymouth Rock may beat GEICO in specific ZIP codes, especially for long-time residents or certain household profiles, GEICO’s broad accessibility and consistent online quoting tools keep it high on many comparison lists. For many New Jersey drivers, GEICO can deliver a useful mix of price, convenience, and dependable coverage options.

🥈 Regional Comparison Pick: NJM Insurance Group

Local experience • Claims reputation • Family-focused coverage options

- Regional strength: deep roots in New Jersey

- Customer service reputation that many shoppers value

- Discounts that may apply for good students, safe drivers, and bundles

- Local market focus for New Jersey policyholders

A trusted regional insurer worth comparing for New Jersey liability coverage

While GEICO often appears as a strong affordability pick, NJM Insurance Group (New Jersey Manufacturers) can also be a strong comparison option for liability-only coverage in the Garden State. Unlike many national carriers, NJM is a regional company with deep roots in New Jersey, giving it local familiarity with driving conditions and risk factors. That focus may translate into competitive premiums for some residents, particularly long-time policyholders and families with clean driving records.

NJM is also praised by many policyholders for customer service and claims handling. The company provides discounts that may apply to bundling, safe driving, and good students, making it especially attractive for households with multiple drivers. For many New Jerseyans, especially in suburban and rural ZIP codes, NJM may offer a more competitive price while providing a more personalized, community-focused experience.

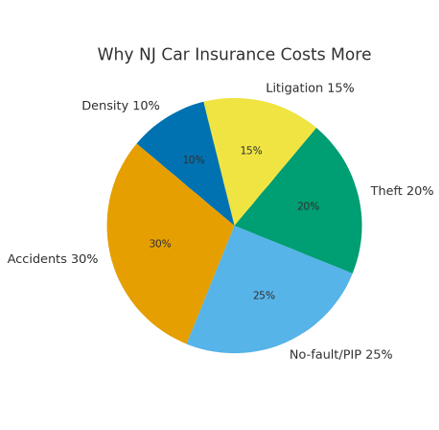

Why New Jersey Car Insurance Costs More

New Jersey ranks among the more expensive states for auto insurance, largely due to a combination of urban density, accident frequency, medical coverage rules, and claims costs. Here are the biggest cost drivers:

- High accident frequency – New Jersey’s highways, such as the Garden State Parkway, NJ Turnpike, and I-95 corridor, are some of the busiest in the region. More traffic can lead to more crashes and higher claims.

- No-fault insurance laws – NJ is a no-fault state, meaning drivers must carry Personal Injury Protection coverage. This can raise costs compared to states without mandatory PIP.

- Urban theft and vandalism – Cities such as Newark, Jersey City, and Paterson may have higher vehicle theft, vandalism, or claims risk, which insurers can factor into premiums.

- Claims and litigation environment – Liability settlements, medical bills, and disputed claims can affect insurer payouts and pricing over time.

- Population density – New Jersey is one of the most densely populated states in the country. More people, more cars, and more congestion can increase risk for insurers.

On average, liability-only coverage statewide may cost around $1,000 to $1,200 annually in many rate studies. But in urban ZIP codes, premiums may be significantly higher unless you shop carefully, maintain continuous coverage, and qualify for discounts.

Factors Driving New Jersey Insurance Costs

| Factor | How It Can Affect Premiums |

|---|---|

| High Accident Frequency | Can increase claim volume and insurer risk |

| No-Fault / PIP Mandates | Can increase medical claim costs |

| Theft & Vandalism | Can raise risk in certain ZIP codes |

| Claims and Litigation Environment | Can increase payout and defense costs |

| Population Density | Can increase congestion and crash exposure |

Liability Insurance for Teen Drivers in New Jersey

Adding a teenager to your auto policy in NJ can sharply increase liability premiums. Teens are high-risk drivers, and insurers adjust rates accordingly. Still, there are strategies to reduce costs:

- Good Student Discounts – Teens who maintain a B average or higher may qualify for reduced rates with some insurers.

- Driver Training Courses – NJ-approved defensive driving or driver training classes may help reduce premiums depending on the insurer.

- Telematics Monitoring – Programs like Progressive’s Snapshot or State Farm’s Drive Safe & Save may reward safe driving behavior.

- Family Policies – Adding teens to a parent’s policy is usually more cost-effective than buying separate coverage.

- Vehicle Choice – A modest, safe, reliable car can help keep liability premiums more manageable.

In New Jersey, companies like State Farm, Progressive, and NJM may be worth comparing for teen drivers, but the best option depends on the teen’s age, household, ZIP code, vehicle, and discount eligibility.

Liability Insurance for Seniors in New Jersey

Seniors in New Jersey may face higher rates after age 70, as insurers can factor in accident severity risks and driving patterns. However, many carriers provide targeted discounts:

- AARP Auto Insurance Program (The Hartford) – Senior-friendly policies may include safe-driving rewards or member-related benefits.

- AAA Northeast – May offer loyalty perks, roadside benefits, or other features that some older drivers value.

- Defensive Driving Discounts – Seniors who take refresher driving courses may qualify for premium reductions with some insurers.

- Low-Mileage Discounts – Retired drivers who use their cars sparingly may qualify for reduced premiums.

Shopping every few years is especially important for seniors, since insurers weigh age and mileage differently. Seniors should also consider raising liability limits beyond the minimums to protect retirement savings and home equity.

Compare Quotes in 2 Minutes

Compare Insurance Quotes and Save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

How to Save Money on Liability Car Insurance in New Jersey

Even within the same county, liability premiums can differ by hundreds of dollars. Smart shopping makes all the difference:

- Get at least three quotes on the same day to compare fairly.

- Bundle auto with homeowners or renters insurance for multi-policy discounts.

- Enroll in telematics programs if you’re a safe driver and comfortable with driving-data tracking.

- Ask whether paying your premium in full is cheaper than monthly installments.

- Maintain continuous coverage to avoid penalties, reinstatement problems, and higher rates.

- Ask about affinity discounts for alumni associations, unions, employers, or professional groups.

- Raise deductibles on optional coverages if you carry more than liability and can afford the out-of-pocket risk.

These tactics apply statewide, but they are especially useful in high-cost areas like Newark, Elizabeth, and Jersey City.

Common Pitfalls to Avoid When Insuring Your Vehicle in NJ

Chasing the cheapest rate sometimes leads drivers into costly mistakes. Here are pitfalls to watch for:

- Ignoring MVC compliance – If your insurer does not properly report coverage or you cannot provide proof of insurance when required, you may face fines, suspension, surcharges, or other penalties.

- Choosing the Basic Policy when you have assets – Minimum limits may leave you exposed after a serious accident.

- Forgetting high-risk or assigned-risk rules – If you have serious violations, suspensions, at-fault accidents, or insurance eligibility points, you may have fewer voluntary-market options and may need to ask about the New Jersey Personal Automobile Insurance Plan (PAIP).

- Overlooking hidden fees – Some low-premium plans add installment, processing, or reinstatement charges that can make them more expensive long-term.

FAQs About Liability-Only Auto Insurance in NJ

For a Standard Policy issued or renewed on or after January 1, 2026, New Jersey minimum liability limits are generally $35,000 bodily injury per person, $70,000 bodily injury per accident, and $25,000 property damage per accident. The Basic Policy is separate and more limited.

No. If your vehicle is registered in New Jersey, it generally must be insured. Contact the NJ MVC or your insurer before canceling coverage on a registered vehicle.

It depends on your profile, but GEICO, NJM, Progressive, State Farm, and USAA if eligible, are often worth comparing. The cheapest company for one driver may not be the cheapest for another.

Usually not. It is often cheaper to add a teen driver to a parent’s policy, but the best option depends on household, vehicle, insurer rules, and eligibility.

Not always. Some seniors may see higher rates with age, but many insurers offer discounts for defensive driving, low mileage, or policy bundling. Comparison shopping is crucial.

The Final Word on Cheap Liability Car Insurance in New Jersey

While New Jersey is one of the more expensive states for auto coverage, cheap liability insurance is still possible with the right approach. By understanding NJ’s unique policy structures, shopping strategically, and taking advantage of discounts tailored for teens, seniors, and safe drivers, you can keep costs manageable without risking fines or underinsurance.

For many drivers, companies like GEICO, Progressive, NJM, State Farm, Plymouth Rock, and USAA, for those who qualify, are worth comparing for liability-only premiums in New Jersey.

Staying compliant with New Jersey law, protecting your financial future, and avoiding unnecessary costs all come down to smart shopping and continuous coverage. With the strategies outlined in this guide, you can look for cheap liability car insurance in NJ and also get coverage that better protects you.

Find cheap liability car insurance in New Jersey today with a custom online quote. Compare quotes from multiple insurers through the Citizens Insurance comparison form, review your coverage options carefully, and look for ways to save on your New Jersey car insurance.

References

- New Jersey Motor Vehicle Commission. Insurance Requirements.

- New Jersey Department of Banking and Insurance. New Jersey’s Basic Auto Insurance Policy.

- New Jersey Department of Banking and Insurance. Standard Auto Insurance Policy.

- New Jersey Department of Banking and Insurance. Bulletin No. 25-06: Auto Insurance Coverage Limits Pursuant to P.L.2022, c.87.

Compare Quotes in 2 Minutes

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

OUR WEBSITE

TRUST & AUTHORITY

Featured Articles

SEARCH

Looking for something specific? Use the search bar below to find answers to your questions!